Your search results [1 article]

The first beer brewing bookkeeping in the world, 5500 years ago.

In the temple of Inanna at Uruk (southern Iraq today), miniature clay jars with pointed bottom and flared neck has been retrieved (h ˜ 3 cm). They were used as tokens for a primitive accounting organised by the sanctuary at the end of the IVth millennium[1].

")

From the underground of the city of Uruk came out about 5000 clay tablets covered with archaic pictograms, written between 3100 and 2900 BC. They are all of an economic character. The oldest are hardly more elaborate than a simple clay tag. They show a numerical sign next to the archaic pictogram of the object counted. Grain-based products, including beer, are mostly indentified or deciphered. See (First writings ).

The numerical operations are simple sums. On the front side of a clay tablet a mark is stamped for each jar of beer. On the reverse side, these numerical signs are juxtaposed in a single box, a simple addition with no upper units. We stay close to the clay tokens enclosed in a bag or a clay capsule: as many jars of beer as there are clay substitutes similar to those pictured above!

Quickly, these primitive records are divided into several boxes to record several products separately or to name people (ration recipients, senders or recipients, sellers or buyers, transaction managers, signatories). However, these better structured documents do not provide any contextual information, not even the date or place where these records have been drawn up.

Fig. 1 : a slip with 2 entries and a signature (H. Nissen et al., 1993: fig 39b).

These primitive accounts detail, on the front side of the clay tablet, various homogeneous deliveries (grains, beer jars, breads, sheep, ...). They give the total on the reverse side. Example Fig. 1 : two totals are written with the signature of the manager. The 120 grain rations and 30 jars of beer summarise the minute distribution operations of grain and beer noted on the obverse side.

The first account was born!

It brings together on the same document several products affected by the same operation (distribution, withdrawal or entry into stocks) and adds up the quantities of each product category. This improvement follows the use of multiples of the unit and the handling of larger numbers. The products are counted with different numerical systems to make a separate calculation and record them separately.

But the scribe also knows how to convert all these volumes into the same accounting unit. The scribes know how to count grain rations, malt, brewing cakes and jars of beer separately. But they also calculate the barley volume equivalent to these products. They forge a reference accounting unit, a sort of "litre"-barley, to add up the grain volume of products of the same origin (bread, galettes, cakes, beer, wort, malt, beer-cake, barley, wheat, ...) but of different qualities (ordinary, strong or weak beer, small or large bread, ...). This accounting unit makes it possible, after the conversion of all the by-products, to compare the barley equivalent of the raw material used (emmer or barley grains) with the barley equivalent of all the manufactured products with it.

Cereal products, grains, bread and beer play a key role in this development. The brewery maintains privileged links with the sphere of writing. This new tool can calculate a ratio "grains consumed"/"beer produced". This ratio reflects the sum up volume of various ingredients used for a batch of beer compared to the volume of the different types of beer brewed and delivered.

This lovely puzzle has been elegantly solved by Mesopotamian specialists! They already know how to record periods of 8 years production and to count volumes of barley in the range of 16,000 litres, as shown by 2 archaic clay tablets which are part of a set found near the city of Kiš[2].

A batch of 18 clay tablets from Uruk reflects this progress at the dawn of the 3th millennium[3]. These are the archives of the SANGA named Ku-šim, administrator of temple or palace and in charge of their brewery. One of his accounts totals 135,000 litres of barley over a period of 37 months, a figure commensurate with his function. Kušim controls the distribution of barley and beer to the officers, the use of malt, and that of the brewing cakes. Two clay tablets deserve to be analysed. They materialize the interaction between the technical processes of the brewery and the evolution of the accounting documents.

The first tablet has a simple structure: a supply of 3052.8 litres of barley consists of 1257.6 litres of cakes and 1795.2 litres of malt (Fig. 2). The total box juxtaposes the numerical signs of the malt and those of the cakes, a proof that these two numerical systems are convertible and can be added together.

")

Fig. 2 : accounting of malt and barley cakes (H. Nissen et al., 1993, fig. 36)

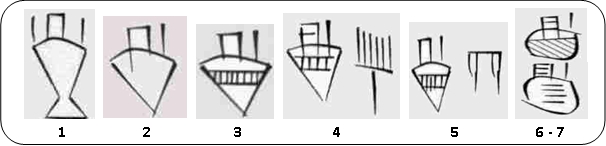

Two "key accounts" are presented as the most elaborate of the series and of all the known clay tablets of this period. The accounting of barley, brewing ingredients and beers generates complex documents. Several types of beer are recorded here. Each can vary in size of the jars or in the ratio of grain to beer:

Fig. 3 no 1-2 = beer grade a (pictogrammes standard)

Fig. 3 n° 3, 6 and 7 = a beer grade b, c or d (standard picto + hatching)

Fig. 3 n° 4 = large jar of beer of grade b (or beer b brewed according according to a high ratio grains/beer)

Fig. 3 no 5 = small jar of beer grade b (or beer b brewed according to a low ratio grains/beer)

Fig. 3 : pictograms of beer jars or designating different grades of beer

In the first of these clay tablets (Fig. 4), the scribe recapitulates the proportions of malt and cakes by grades of beer and/or barley by type of grain products.These "analytical" accounts provide valuable information on the composition of Mesopotamian beers.

Fig. 4 : malt, brewing cakes and beer jars (H. Nissen et al., 1993, fig. 38)

Fig. 4 : malt, brewing cakes and beer jars (H. Nissen et al., 1993, fig. 38)

For example, 5 large jars of beer (beer no. 4 according to Fig. 3) require 36 l of cake and 36 l of malt. But 30 small jars of beer (beer no. 5 according to Fig. 3 require 86,4 l of cake and the same amount of malt. The beer being of the same type b, and if we suppose that

This clay tablet gives a ratio for each type of beer. For 120 jars of beer of the type c, you need 172.8 l of cakes and the same amount of malt. For 60 jars of type a

With the second large clay tablet (Fig. 5a = recto et 5b = verso), the accounting mastery reaches a peak. All the achievements are being implemented, with four improvements:

a) accounting collation based on series of small receipts

b) concept an record of the calculation period

c) grand total by ingredient for the recorded period

d) cumulative figures by grades of beer for the recorded period

Fig. 5a : FRONT side of a collation with grand totals (H. Nissen, 1993, fig. 39)

On the front side, the data of small slips are shown in 3 columns (e.g. a slip Fig. 1) or other clay tablets for the distribution of jars written by different departments or officials (e.g. Fig. 2). Luckily, we have one of those tablets used to collate our large clay tablet. It records the number of jars of different beers allocated to 4 persons, the names of the brewers and their working time[4].

Fig. 5b : Back side of the collation fig. 5a and grand totals (H. Nissen, 1993, fig. 39)

It was thus possible to control that a distribution to one of the 4 beneficiaries is completely recovered by the large clay tablet (5 large jars n° 4, 10 small jars of beer n° 5, 20 jars of beer n° 6-7 after Fig. 3). This tablet records the beer jars of grades a, b, c dispensed for various purposes including religious celebrations or offerings. The name of the city goddess of Uruk appears in a box (bottom right box, Inanna) Fig. 5a).

These clay tablets illustrate the practice of deferred accounting. Small clay tablets record the output of brewing ingredients and the distribution of the corresponding beers. These minute records written on spot are kept and later used to establish general accounts (Fig. 5a : FRONT SIDE). The volumes of brewing ingredients consumed and jars of beer delivered over a certain period of time are then added up and approved by a high-level official (Fig. 5b : BACK SIDE). The conversion of the volumes of brewing ingredients and beers into a grain-barley equivalent allows the brewing ratios to be controlled.

These accounting mechanisms are part of an economic organisation. One entity, both administrative and physical ( warehouses, malting areas, brewing workshops) is responsible for supplying the barley, another for manufacturing the brewing ingredients (malt, bappir, cake), a third one for brewing the beers, and a last one for distributing the beer jars to the staff. All these operations, duly recorded on "small clay tablets", are then summarised by the scribes on periodic large accounts. At that time, the brewery's accounts were already based on two procedures: firstly, recording and noting the products on slips on the spot in the brewing workshops; secondly, taking these slips back, adding up and breaking down the volumes managed by type of product (grains, beer jars) and quality of beverage.

One remains amazed by the complexity of these documents and calculations reached from the dawn of the 3th millennium, only a few centuries after the birth of writing. The management imperatives of the brewery play an obvious role in this achievement. Certain essential features of Mesopotamian accounting practice are settled and will remain in force for the next two millennia. Information will become richer, cuneiform writing will move away from pictography, numerical systems will become simpler. But accounting summaries will remain unchanged, especially for the management of brewery, its numerous brewing ingredients and grades of beer.

The principle of a common unit volume of account for the raw grains, brewing ingredients and various beer qualities has been established. It meets the early needs of the brewery, whose process is to be controlled from start to finish, from the initial allocation of the grains to the production of the beer jars. Supervision by the ratio "volume of barley consumed / final volume of beer brewed" is in its infancy in the archaic clay tablets. It will reach its full development during the 3th millennium.

The brewery intendant Ku-Shim who signed off on the above accounts is also the signatory of a record that summarises 37 months of barley supply to the brewery. His name can be read with the 2 pictoes in the top left corner. (bar = KU, beer jar = ŠIM). The recorded volume of barley is 135,000 litres!

This gives an idea of the quantities of grain consumed in the town of Uruk in the 31st century BC. This small clay tablet could be dated thanks to the rapid development of writing styles at that time (forms of pictograms and structures of documents). This record also gives a measure of the economic role of the brewery in the emergence of the first city-states in mankind's history.

[1] Denise Schmandt-Besserat 1988, Tokens at Uruk, Baghdader Mitteilungen 19, 2-35, 42

[2] Hans Nissen, Peter Damerov, Robert Englund 1993, Archaic Bookkeeping. Early Writing and Techniques of Economic Administration in the Ancient Near East, p. 35.

[3] Hans Nissen & al., op. cit. 36-46.

[4] Hans Nissen & al., op. cit. 43-46, et fig. 39 b.